Bring that big benefits energy to your clients.

Healthier teams go further.

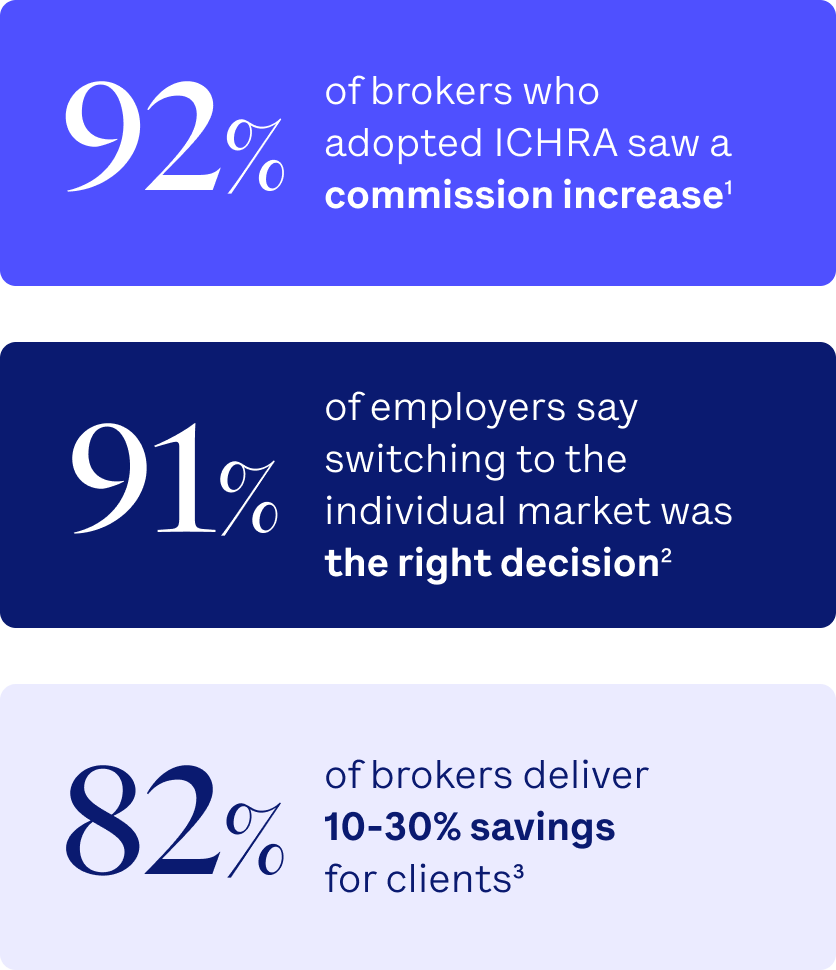

Big moves lead to a bigger book.

Make the change.

Sticky platform + multiproduct selection relationship = longer retention. Grow each employee policy over time.

Step 1

Select an ICHRA administrator

The right platform does the heavy lifting so you and your clients don’t have to.

Step 2

Define contributions

Help clients decide on budgets for part-timers, contractors, or execs. Commissions stack per employee across product lines, not just a group policy.

Step 3

Design the plan

Clients apply dollars to premiums or a full range of care. Build tailored designs to boost value and close rates. Sell standalone or supplemental for year-round income.

Step 4

Launch to employees

Quick, smooth, and easy onboarding. Stop bidding out group plans annually. Employees re-enroll in the ACA while you keep the client through carrier and life changes.

Step 5

Automatic reimbursements

Platforms handle premium reimbursement based on your client’s contribution model. No admin lifts for you.

The right enrollment platform makes a difference.

- Built in compliance

Automatic IRS, ERISA, and HRA guardrails.

- Easy management

Simple workflows, clear reporting, and flexible fees for brokers and employers.

- Guided enrollment

Smart tools that help employees easily choose plans.

- Seamless payments

Fast, reliable reimbursements and automated processing.

- Flexible growth

Syncs with HR/payroll systems and scales as your business grows.

Take a deep dive.

- Wait, what is ICHRA?

ICHRA means Individual Coverage Health Reimbursement Arrangement. It’s a new type of Health Reimbursement Arrangement (HRA) created in 2020. It’s great because it allows businesses of any size to provide tax-free reimbursements to employees for health insurance premiums and qualified medical expenses.

- So, how does ICHRA work?

In most cases, an employer works with a third party (broker and/or ICHRA administration platform) to design and implement their company’s ICHRA. This process typically requires the employer to determine their budget, decide which employees can and cannot participate in the ICHRA, and establish when to launch the new health benefits solution to employees. Once the ICHRA is introduced to the company, employees get to shop for an individual insurance plan on the open market and buy a plan that suits their unique needs. Then, employees seek tax-free reimbursements from their employer each month.

- Who can use ICHRA?

Employers of any size can offer an ICHRA so long as they have at least one employee who isn’t a self-employed owner or the spouse of a self-employed owner. If designed correctly, an ICHRA satisfies the Affordable Care Act (ACA) employer mandate for Applicable Large Employers (ALEs). To determine if ICHRA is right for your business, take a look at the official IRS ICHRA regulations or talk to a tax professional.

- Does ICHRA satisfy the Affordable Care Act (ACA) employer mandate for Applicable Large Employers (ALEs)?

Yes. If designed correctly, an ICHRA satisfies the Affordable Care Act (ACA) employer mandate for Applicable Large Employers (ALEs). To determine if ICHRA is right for your business, take a look at the official IRS ICHRA regulations or talk to a tax professional.

- Can employers offer both an ICHRA and a traditional group health insurance plan to employees?

Hmm, yes and no. Here’s why: Employers can offer an ICHRA to one segment of employees while offering a traditional group plan to a different segment of employees. However, employers are not allowed to offer both an ICHRA and a traditional group plan to the same segment of employees. To determine allowable class distinctions, just refer to official IRS ICHRA regulations or talk to a tax professional.

- What’s the difference between an ICHRA and a traditional HRA?

Historically, HRAs were offered as a tax-advantaged supplement to traditional group insurance as a way to cover qualified medical expenses not included in traditional insurance. However, these HRAs did not allow for tax-free reimbursements to apply towards health insurance premiums. New regulations stipulate that with an ICHRA (as well as QSEHRA), an employer can reimburse for both qualified medical expenses, and health insurance premiums.

- What’s the difference between ICHRA and QSEHRA?

There are many distinctions between these two types of HRAs, but the two primary distinctions are contribution limits and participation sizes. The Qualified Small Employer HRA (QSEHRA) has limits on how much an employer can reimburse their employees while ICHRA has no limitations on the contribution amount.

Additionally, only companies with less than 50 employees can offer a QSEHRA, while an ICHRA can be offered by a company of any size. To understand the complete list of differences between these two types of HRAs, just refer to official IRS regulations or talk to a tax professional.

- Are there limitations to employer contributions with ICHRA?

No. There are no limitations here.

- Do ICHRA benefits cover qualified medical expenses?

Yes. If the employer chooses to allow reimbursement for such expenses, employees can seek reimbursement. During the ICHRA design stage, employers have a choice whether or not to allow the ICHRA to cover qualified medical expenses. To see a complete list of qualified medical expenses, please refer to official IRS ICHRA regulations or talk to a tax professional.

- How does ICHRA work with Premium Tax Credits?

- Is a third-party administrator (TPA) required for ICHRA management?

No, it’s not a legal requirement. That said, it is strongly advised to administer an ICHRA through a third party to ensure compliance with IRS regulations such as HIPAA. To learn more about ICHRA compliance, please refer to official IRS ICHRA regulations or talk to a tax professional.